Understanding settlement types

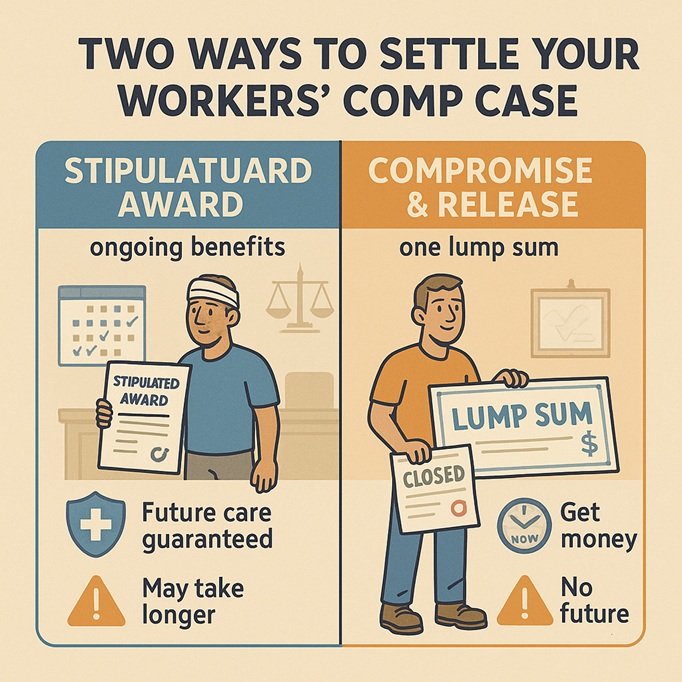

Before you negotiate a workers' comp settlement, you need to know how the money actually arrives. Most cases resolve through one of two payment structures: a lump-sum settlement or a structured settlement. Your choice determines how quickly you access funds and how long the insurance company remains liable for your care.

Lump-sum settlements

A lump-sum settlement provides a single, one-time payment that closes your case permanently. This is the most common outcome for workers seeking immediate financial stability. You receive the full agreed-upon amount upfront, allowing you to pay off medical debts, cover living expenses, or invest for the future without waiting.

The trade-off is finality. Once you accept a lump sum, you typically waive your right to any future benefits related to that injury. If your condition worsens or you require additional surgeries years later, you cannot return to the insurance carrier for more money. This option works best when your medical needs are fully understood and your long-term prognosis is stable.

Structured settlements

A structured settlement distributes payments over a set period, such as weekly, monthly, or annually. Instead of a single check, you receive regular installments that can last for months or years. This approach is often used when long-term medical care is expected but not yet fully quantified.

This method provides a steady income stream, which can help manage chronic pain or disability without the risk of spending a large sum too quickly. However, it also means the insurance company retains control over the funds for the duration of the agreement. You remain dependent on their payments, and if the company faces financial trouble, there may be risks to receiving your full share.

Review your medical records

Before you sign anything, you need to verify that the settlement offer reflects the true cost of your injury. Insurance adjusters use your medical history to calculate the value of your claim. If your records are incomplete or inaccurate, you could accept far less than you deserve.

Gathering and organizing these documents is the most important step in protecting your rights. A complete file shows the full scope of your treatment, from the initial emergency room visit to ongoing physical therapy. It also provides the evidence needed to justify future care costs, which are often the largest part of a workers' comp settlement.

Follow this sequence to ensure your file is complete and accurate.

Request a complete copy of your medical records from every provider involved in your care. This includes your primary care physician, specialists, physical therapists, and any hospitals where you received treatment. Do not rely on summaries; you need the full narrative of your recovery. This documentation forms the backbone of your settlement negotiation, proving the severity of your injury and the necessity of your treatment.

Ensure that all imaging reports (X-rays, MRIs, CT scans) and diagnostic test results are included in your file. These objective pieces of evidence are critical for establishing the extent of your injury. Adjusters often scrutinize these reports to determine if your condition is permanent or if it will fully heal. Having clear, unambiguous diagnostic evidence strengthens your position significantly.

Gather a complete log of all prescriptions filled for your work injury. This includes pain management medications, muscle relaxers, and any other drugs prescribed during your recovery. This history helps establish the timeline of your pain and the intensity of your suffering. It also provides evidence of the ongoing nature of your condition, which is essential for claiming future medical expenses.

If your doctor has determined that your injury has reached maximum medical improvement (MMI), request a formal impairment rating. This rating, often expressed as a percentage, quantifies the permanent damage to your body. It is a key factor in calculating the final value of your workers' comp settlement. Without this official rating, the insurance company may undervalue your claim by assuming you have fully recovered.

A thorough review of these records ensures that no detail is overlooked. Use the checklist below to verify that your file is complete before engaging in final negotiations.

-

Doctor's final MMI report

-

All imaging results (X-ray, MRI, CT)

-

Prescription and medication history

-

Future treatment estimates

Missing even one of these components can leave money on the table. Take the time to be meticulous now, so you can move forward with confidence.

Calculate your total damages

Before you enter negotiations, you need a clear baseline for your workers' comp settlement. This baseline is the sum of your economic losses and non-economic damages. Think of this calculation as building a ledger that proves exactly what the injury has cost you, both financially and physically.

Add up your medical expenses

Start with the hard costs. Gather every bill related to your workplace injury, including emergency room visits, hospital stays, doctor appointments, and prescription medications. Do not forget future medical care. If your doctor indicates you will need ongoing therapy, physical rehabilitation, or future surgeries, these projected costs must be included in your total. Insurance adjusters will scrutinize these numbers, so keep detailed records of every invoice and receipt.

Factor in lost wages

Next, calculate your lost income. This includes wages you missed while recovering from the initial injury. It also covers any long-term disability or reduced earning capacity if you cannot return to your previous job or if your salary has decreased due to permanent limitations. Use your pay stubs, tax returns, and employment contracts to document exactly how much income you have lost or will lose because of the accident. This figure forms the backbone of your economic damages.

Estimate pain and suffering

Pain and suffering covers the non-monetary impact of your injury. This includes physical pain, emotional distress, loss of enjoyment of life, and any permanent scarring or disfigurement. While there is no fixed formula for these damages, they are often calculated as a multiple of your medical expenses and lost wages, or based on the severity and duration of your recovery. This is the most subjective part of the calculation, so it is wise to consult with a legal professional to ensure you are not undervaluing your suffering.

Review your total

Once you have added these components together, you have your total damages. This number serves as your starting point for negotiation. Remember that the insurance company will likely offer less than this total, so having a well-documented, comprehensive calculation gives you the leverage to push for a fair settlement that truly reflects the full extent of your losses.

Spot red flags in settlement offers

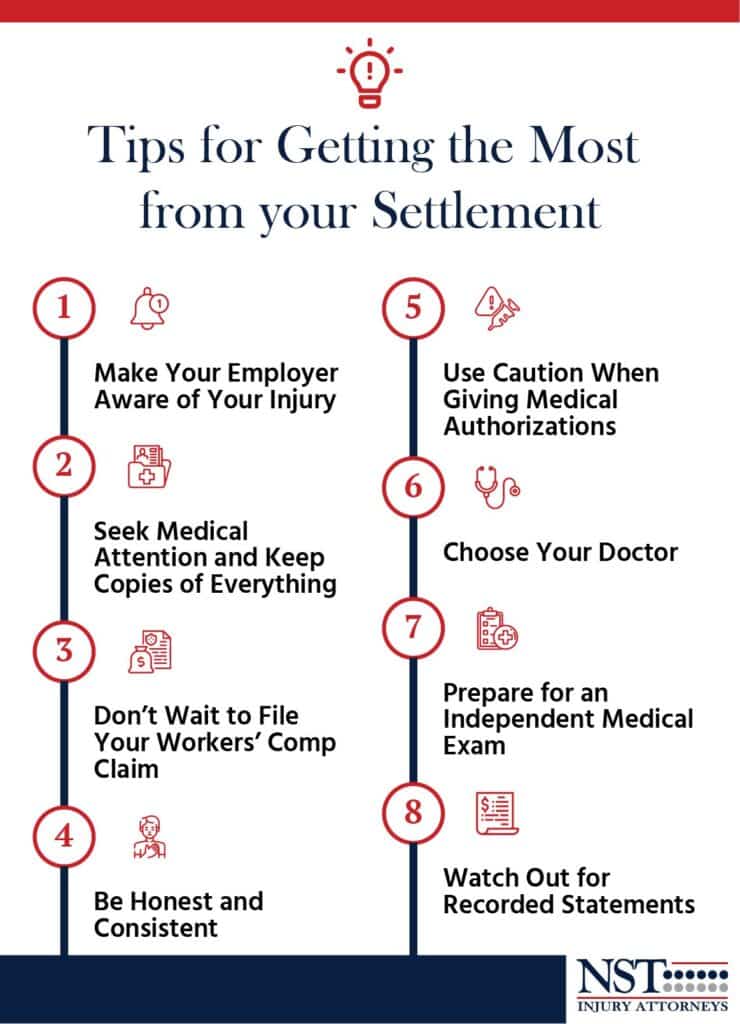

When an insurance adjuster presents a workers' comp settlement, the goal is often to close the case quickly and permanently. A signed agreement typically means the insurance company is no longer responsible for paying any additional medical bills or wage replacements, even if your condition worsens later. This finality requires you to scrutinize every line item before signing.

The most critical error injured workers make is accepting an offer that excludes future medical care. If your doctor indicates you will need ongoing therapy, physical rehabilitation, or potential surgeries down the road, the settlement must explicitly cover those costs. An offer that stops at current expenses leaves you vulnerable to devastating out-of-pocket bills if complications arise. Never accept an offer that does not explicitly cover future surgeries or ongoing therapy related to the workplace injury.

Another common trap is undervaluing your disability rating. Insurers may rely on an initial medical evaluation that doesn't fully capture the long-term impact of your injury. If the settlement amount seems low compared to the severity of your permanent impairment, it may be based on an inaccurate rating. You have the right to request a second opinion or independent medical examination to verify the extent of your disability before agreeing to a figure.

Finally, watch for language that waives your right to appeal or challenge the settlement terms later. Once you sign, you generally cannot go back to court if you realize the deal was unfair. Ensure the document clearly outlines all benefits being provided, including lump-sum payments and any structured annuity options, so there are no hidden exclusions.

Finalizing the agreement

Before you sign anything, ensure the settlement contract matches every term you and your attorney negotiated. This is your last chance to catch errors in the payment amount, medical coverage details, or the specific release of claims language. Once you sign, the case closes completely, meaning the insurance company will not be responsible for paying any additional costs related to your injury, even if your condition worsens later.

After reviewing the document, you will sign the release of claims. This legal step transfers your right to future compensation for this specific incident to the insurance carrier in exchange for the agreed-upon lump sum or structured payments. Keep a copy of the signed release for your personal records, as it serves as proof that the debt has been satisfied.

Finally, you will receive the settlement funds. Be aware that while workers' compensation settlements are generally tax-free, portions of a settlement can be taxable if they include back pay or interest. Consult a tax professional to report the income correctly on your federal return. If you have outstanding medical liens, those amounts will be deducted from the total before you receive your net payment.

Common settlement: what to check next

Workers' compensation settlements vary widely based on injury severity, jurisdiction, and whether medical expenses are ongoing. Understanding the typical ranges and what reduces your final payout helps set realistic expectations.

No comments yet. Be the first to share your thoughts!