How settlement values change in 2026

Workers' compensation settlements are not fixed sums; they are calculated based on a complex mix of state statutes, medical necessity, and wage history. In 2026, the final payout amount for injured workers in Florida and Nevada depends heavily on recent legislative adjustments that alter how disability benefits and medical expenses are valued. Understanding these baseline calculations is essential before reviewing specific state rules.

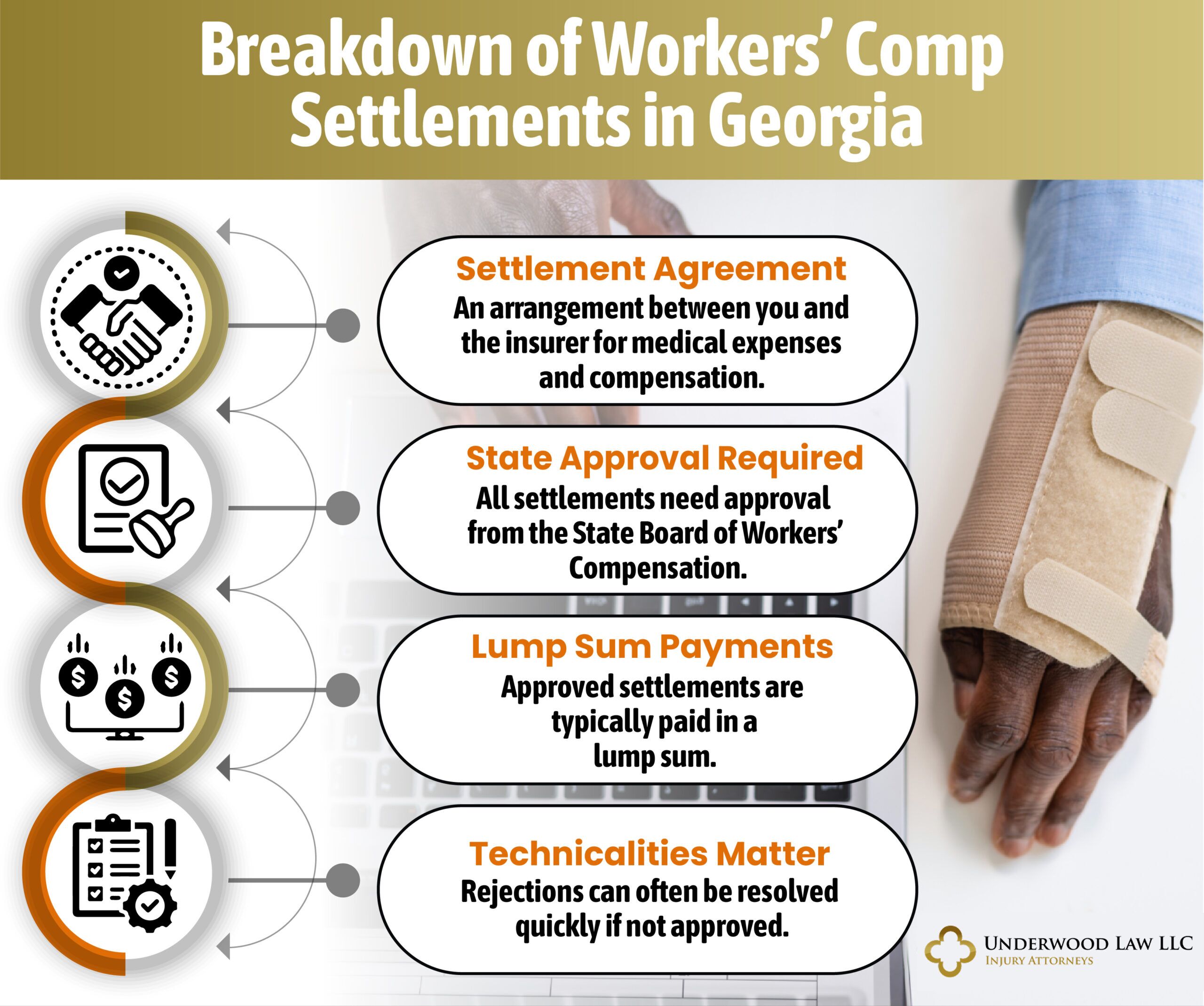

At their core, most settlements cover economic damages, including lost wages and future medical care. As noted by industry sources, the majority of cases resolve through structured settlements—either a lump sum or weekly payments—designed to cover a pre-determined period of disability [The Hartford]. However, the "pre-determined" nature of these payouts varies significantly by jurisdiction. In Florida, the value is tightly bound to average weekly wage calculations, while Nevada relies on specific injury schedules that assign fixed values to particular body parts.

Recent updates in both states aim to standardize these calculations, reducing ambiguity for employers and employees alike. In Florida, adjustments to the maximum weekly benefit caps directly impact the total compensation available for long-term disability. Meanwhile, Nevada’s 2026 updates refine how permanent partial disabilities are assessed, ensuring that the scheduled loss aligns more closely with modern medical understandings of recovery and function.

These legislative shifts mean that a settlement offer in 2026 may look different than it did in previous years, even for similar injuries. For injured workers, this underscores the importance of accurate wage documentation and comprehensive medical records. For employers, it highlights the need to stay current with statutory rate changes to ensure compliance and fair valuation. The interplay between these state-specific rules creates a distinct landscape for settlement negotiations, where precision in calculation is paramount.

Florida workers comp settlement factors

Florida’s workers’ compensation system relies on strict statutory formulas to determine settlement value. Unlike fault-based personal injury claims, these settlements are primarily driven by the severity of the injury and the worker’s pre-injury earnings. Understanding how Temporary Total Disability (TTD) and Permanent Partial Disability (PPD) are calculated is essential for evaluating any offer.

Temporary Total Disability benefits replace a portion of your lost wages while you are unable to work during recovery. In Florida, this rate is typically two-thirds of your average weekly wage, subject to a state-mandated maximum cap set annually. These payments continue until you reach maximum medical improvement (MMI) or are cleared to return to work. If your injury prevents you from returning to your previous job, you may also qualify for Temporary Partial Disability (TPD) or vocational rehabilitation benefits.

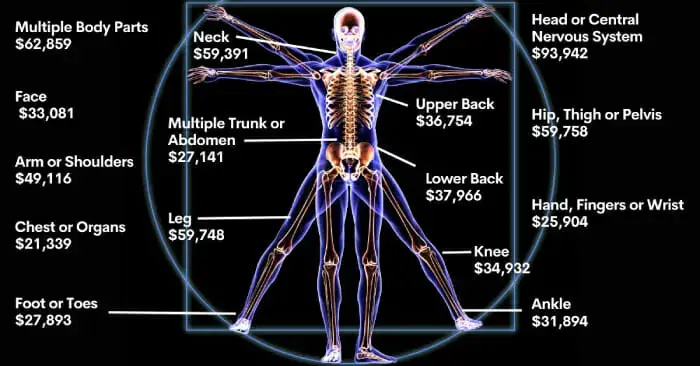

Once you reach MMI, the focus shifts to Permanent Partial Disability (PPD). Florida uses a "schedule" for specific body parts—such as arms, legs, eyes, and ears—assigning a set number of weeks of benefits based on the percentage of impairment. For non-scheduled injuries, like back or neck strains, the calculation depends on the impact on your earning capacity. The 2026 updates to Florida workers’ comp laws continue to emphasize these structured calculations, ensuring payouts align with statutory caps rather than subjective negotiation.

The calculator above provides a baseline estimate for TTD or scheduled PPD benefits. It applies the standard two-thirds wage replacement rate to your weekly earnings over the specified duration. Note that this figure does not account for attorney fees, medical liens, or the specific impairment rating assigned by a qualified physician, which can significantly alter the final settlement amount.

Nevada Workers Comp Settlement Factors

Nevada handles workers' compensation settlements differently than many other states, relying heavily on a statutory schedule of injuries to determine value. This schedule assigns specific monetary values to different body parts and injuries, creating a more predictable, though sometimes rigid, framework for resolving claims. Understanding these statutory benchmarks is essential for evaluating any offer.

Statutory Schedules and Injury Valuation

Nevada law provides a detailed schedule that assigns point values or specific dollar amounts to various injuries, such as the loss of a limb or hearing. These schedules serve as the baseline for calculating settlement amounts, ensuring consistency across cases. However, they do not always capture the full scope of an injured worker's unique circumstances, such as long-term care needs or lost earning capacity beyond the scheduled value.

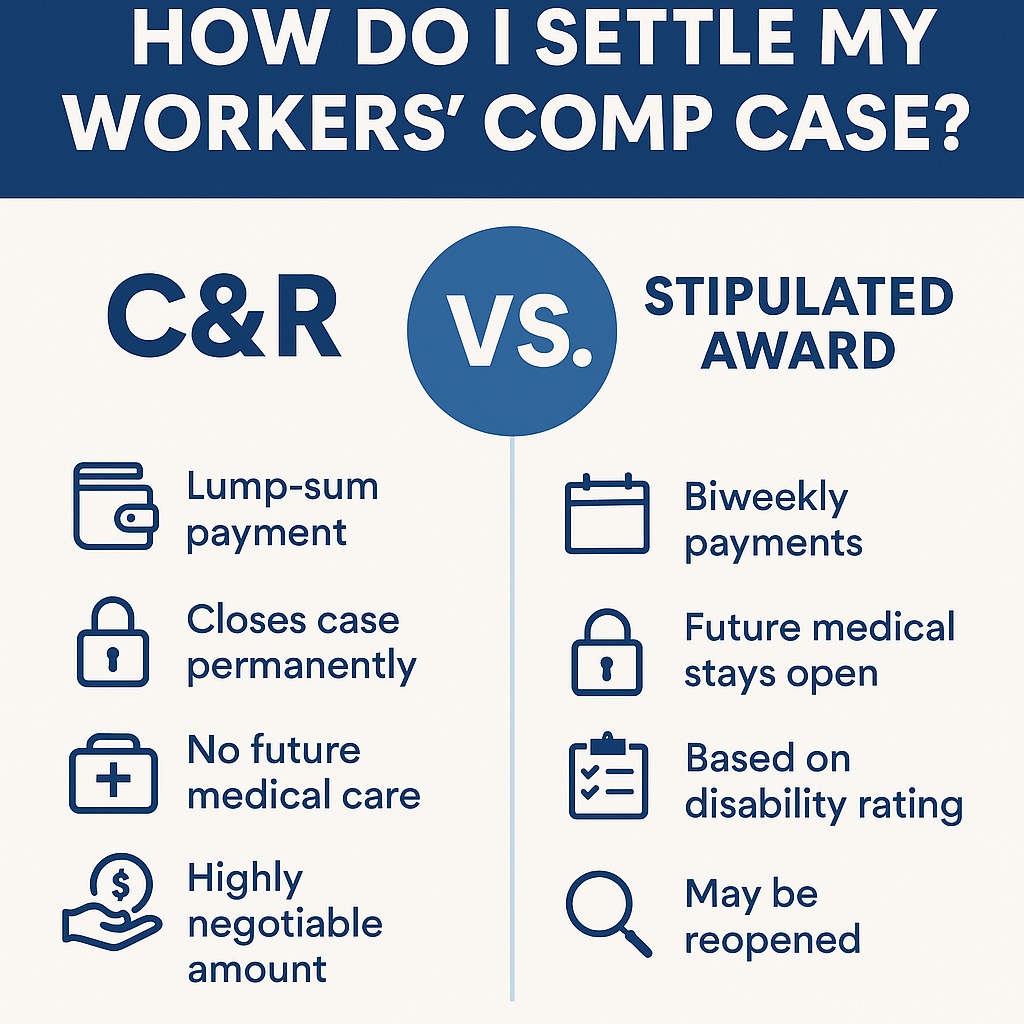

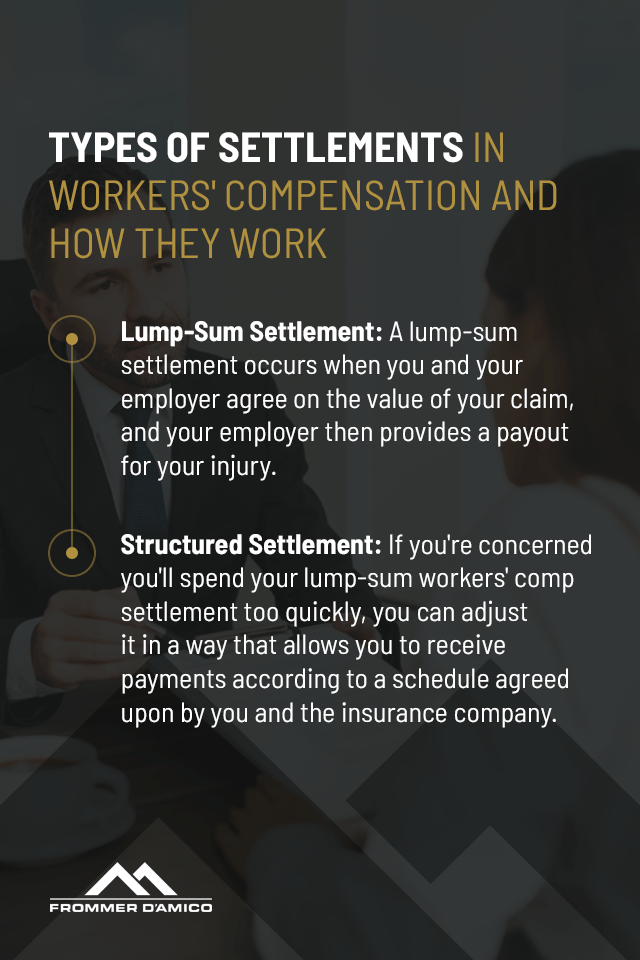

Lump-Sum vs. Structured Payments

Injured workers in Nevada typically have the option to choose between a lump-sum settlement or structured periodic payments. A lump-sum provides immediate access to funds, which can be useful for paying off debts or covering immediate medical costs. Structured payments, on the other hand, offer a steady income stream that can provide long-term financial stability, particularly for those with permanent disabilities that affect their ability to work.

2026 Legislative Changes

Legislative updates in 2026 have introduced modifications to how these benefits are calculated and distributed. These changes may affect the maximum allowable settlements for certain injury types or alter the criteria for qualifying for structured payments. It is critical to review the latest statutory language to understand how these adjustments impact the potential value of your specific claim.

Comparing Settlement Structures

The following table highlights the key differences between how Florida and Nevada approach settlement structures, helping you understand the unique advantages and limitations of Nevada's system.

| Feature | Nevada | Florida |

|---|---|---|

| Settlement Basis | Statutory schedule of injuries | Negotiated based on disability rating |

| Payment Options | Lump-sum or structured | Mostly lump-sum |

| Legal Framework | NRS Chapter 616 | Florida Statutes Chapter 440 |

How to calculate your estimated settlement

Understanding the math behind a workers' compensation settlement helps you prepare for negotiations in Florida and Nevada. While every case is unique, the final amount generally follows a predictable structure based on statutory formulas and documented losses. Think of the settlement process like a pie chart: the whole pie is divided into specific slices representing different types of damages, and each slice has its own rules for calculation.

The first slice is usually the most significant: compensation for lost wages. In both Florida and Nevada, this is often calculated as a percentage of your average weekly wage (AWW) prior to the injury. Nevada typically offers two-thirds of your AWW, subject to state maximums, while Florida uses a similar two-thirds formula but with different caps depending on the disability duration. This component ensures you receive a portion of your income while you are unable to work.

The second slice covers medical expenses. This includes all reasonable and necessary costs related to your injury, such as hospital visits, surgery, physical therapy, and prescription medications. In many settlements, especially those involving permanent impairment, future medical care is estimated and included in the lump sum. It is critical to keep detailed records of all treatments, as these documents serve as the evidence for this portion of the claim.

The final slice accounts for permanent impairment or disability. If your injury results in a lasting limitation, you may be entitled to additional compensation based on the American Medical Association (AMA) Guides or state-specific schedules. This is where the complexity increases, as the degree of impairment is assessed by a medical professional and then converted into a monetary value using state guidelines. The calculator below provides a rough estimate based on these standard components.

Common questions about workers' comp settlements

Workers' compensation payouts vary significantly based on injury severity, state laws, and outstanding debts. In Florida and Nevada, the final amount you receive depends on how liens and fees are handled. Below are answers to the most frequent questions about settlement quality and net payouts.

Next steps for your claim

Before entering settlement negotiations or meeting with an attorney, organize your documentation to strengthen your position. A clear paper trail reduces ambiguity and helps insurers evaluate the true cost of your injury. Gather all medical records, bills, and correspondence related to the workplace accident. Keep a log of missed workdays and any out-of-pocket expenses, such as transportation to medical appointments.

Consider using a workers' comp calculator to estimate potential settlement ranges based on your lost wages and medical costs. This baseline helps you recognize lowball offers early. Remember that most settlements include deductions for attorney fees and outstanding medical liens, so the final payout may be lower than the gross settlement amount. Understanding these deductions prevents unpleasant surprises later.

Carefully compare the offer against your documented damages. Check if it covers all past and future medical expenses, not just current bills. If the offer excludes future care for a chronic condition, it is likely insufficient. Do not sign any release forms until you are certain all liabilities are addressed.

Bring your organized files and calculator estimates to a qualified attorney. They can identify hidden liabilities, such as third-party claims or insurance liens, that might reduce your net recovery. An attorney ensures the settlement structure—whether lump sum or structured payments—aligns with your long-term financial needs.

Once you accept an offer, review the final settlement agreement for accuracy. Ensure all names, dates, and amounts match your understanding. After signing, the insurer will process the payment, which may take several weeks. Keep a copy of the signed agreement and proof of payment for your records.

No comments yet. Be the first to share your thoughts!